Staying the course

Summary

- The Reserve Bank of New Zealand Monetary Policy Committee decided to hold the line, keeping the Official Cash Rate at 5.5% and maintaining an Official Cash Rate outlook similar to its November forecasts.

- It appears the RBNZ now has a more balanced view on inflation pressures than its ultra-vigilant November statement and subsequent communications had led us to believe.

- We expect the Monetary Policy Committee will be able to begin cutting the Official Cash Rate by the second half of 2024 as a weaker economy, waning global inflation, and easing labour market take pressure off domestic inflation.

On hold

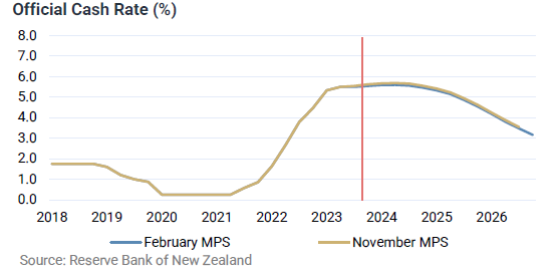

The Reserve Bank of New Zealand (RBNZ) Monetary Policy Committee (MPC) maintained the Official Cash Rate (OCR) at 5.5%, as we expected. This expectation was shared by most investors and economists.

The real interest was in the RBNZ’s forecasts, particularly the OCR and inflation forecasts, to get a sense of the MPC’s possible future moves. The RBNZ continues to see the current OCR level being maintained until at least the middle of 2025. While the possibility of an OCR hike was hinted at if inflation does not head in the right direction fast enough, the Reserve Bank Governor and MPC did not dwell on this to the extent they did at the November meeting.

More balanced inflation outlook

Overall, the record of the MPC discussion appeared more balanced than its November deliberations. The Committee noted that supply and demand have come into better balance, which is easing upward pressure on prices. Below trend global economic activity and lower prices for our exports have also played a role in easing inflation. However, the MPC noted that poor productivity had lowered New Zealand’s potential economic growth rate, which partly offsets the disinflation from other factors.

At its November meeting, the MPC highlighted the risks to inflation from the recent surge in net inward migration. At today’s meeting, the MPC seemed to have a more balanced view of migration. While recognising the impact on demand, particularly the effect on rent inflation, the MPC also highlighted the increase in labour supply and easing of labour market pressures coming from the increase in migration.

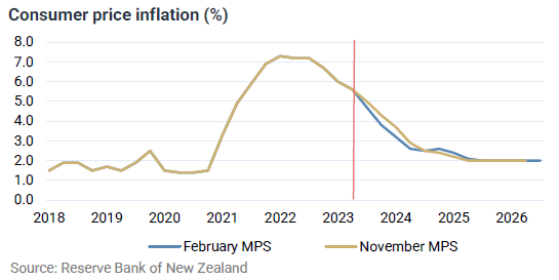

The RBNZ inflation forecasts are marginally lower for 2024 compared to its November predictions. Inflation declines to within the 1-3% target band by the September quarter 2024 and around the middle of the target band by the September quarter 2025.

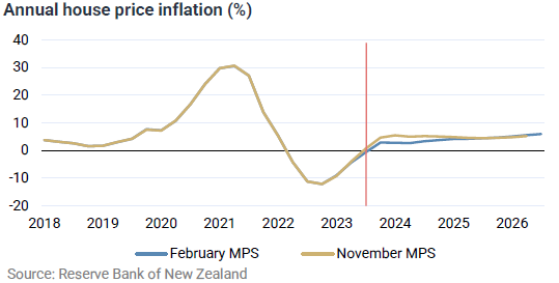

A key reason given by the RBNZ for its lower inflation forecast over 2024 is lower house price inflation than it previously expected. It now expects house price inflation to a relatively modest 5% over 2024 and remains relatively muted over the rest of its forecast period out to 2026. The RBNZ assess that the lagged impact of recent monetary policy tightening continues to restrain the housing market recovery, despite ongoing additional demand via high net immigration.

Little tolerance for upside inflation surprises

The RBNZ forecasts and Monetary Policy Statement commentary suggest the MPC has a more balanced view around future inflation risks than its communications had led us to believe beforehand. Nevertheless, the MPC warn that the economy may have a low tolerance for upside inflation surprises in that this may entrench expectations of higher future inflation. This would make it harder for the RBNZ to achieve and maintain its 1-3% inflation target. Therefore, the RBNZ may need to raise the OCR if this occurs.

We expect OCR cuts later this year

For now, the possibility of another OCR hike has not been factored into the RBNZ’s forecasts. Consequently, financial markets have interpreted the MPC’s stance as less aggressive than previous thought, with wholesale interest rates falling significantly on the announcement and release of its statement.

We continue to expect the RBNZ will be in a position to begin cutting the OCR in the second half of 2024 for several reasons including a weak New Zealand economy, rapidly waning global inflation, and an easing labour market.

John Carran is an Investment Strategist and Economist and John Norling is Director, Head of Wealth Research at Jarden. The information and commentary in this article are provided for general information purposes only. It reflects views and research available at the time of publication, using external sources, systems and other data and information we believe to be accurate, complete and reliable at the time of preparation. We make no representation or warranty as to the accuracy, correctness and completeness of that information, and will not be liable or responsible for any error or omission. It is not to be relied upon as a basis for making any investment decision. Please seek specific investment advice before making any investment decision or taking any action. Jarden Securities Limited is an NZX Firm. A financial advice provider disclosure statement is available free of charge here.